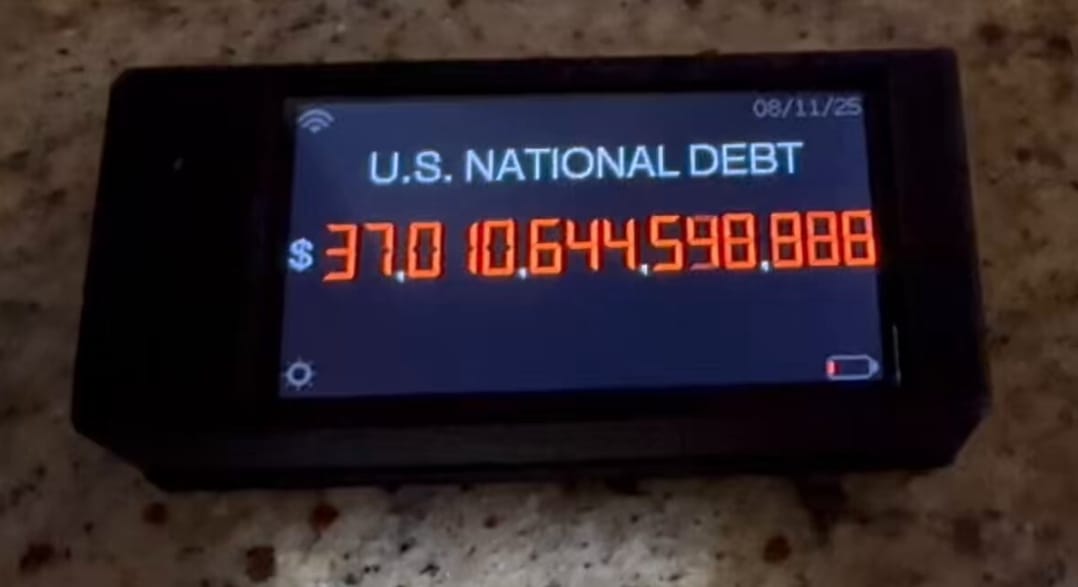

The United States’ national debt has officially surpassed $37 trillion, marking a historic high reached years earlier than expected, according to the Treasury Department’s latest report confirmed to FOX5 Las Vegas.

The milestone comes well ahead of the Congressional Budget Office’s (CBO) January 2020 forecast, which projected the debt would reach this figure after fiscal year 2030. The faster-than-expected rise is attributed to a combination of pandemic-era borrowing and subsequent legislative measures, including the recently passed One Big Beautiful Bill, which is set to add an estimated $4.1 trillion to the debt over the next decade.

Treasury figures released Tuesday show the national debt topping $37 trillion, underscoring the rapid pace of borrowing since the COVID-19 pandemic began in 2020. Under both former President Joe Biden and President Donald Trump (first term), the federal government borrowed heavily to stabilize the economy during shutdowns and to fund recovery efforts.

Michael Peterson, Chair and CEO of the Peter G. Peterson Foundation, warned that the accelerating debt “puts upward pressure on interest rates, adding costs for everyone and reducing private sector investment,” while crowding out other priorities in the federal budget.

The U.S. has hit a string of trillion-dollar milestones at record speed — $34 trillion in January 2024, $35 trillion in July 2024, and $36 trillion in November 2024. “We are now adding a trillion more to the national debt every five months,” Peterson noted, “more than twice as fast as the average rate over the last 25 years.”

Economic experts also point to long-term fiscal strain. Wendy Edelberg, a senior fellow at the Brookings Institution, stressed that the Republicans’ tax and spending legislation means “we’re going to borrow a lot over the course of 2026, we’re going to borrow a lot over the course of 2027, and it’s just going to keep going.”

The Government Accountability Office warns rising debt could drive up borrowing costs for mortgages and car loans, lower wages, and increase the price of goods and services.

At the current daily rate of growth, the Joint Economic Committee estimates the debt could rise by another trillion dollars in roughly 173 days.

Maya MacGuineas, president of the Committee for a Responsible Federal Budget, called the $37 trillion mark a wake-up call: “Hopefully this milestone is enough to wake up policymakers to the reality that we need to do something, and we need to do it quickly.”

Credit: @FOX5Vegas via X.

Leave a Reply